As the 2022 holiday shopping season approaches, we face an unprecedented economic environment. Inflation remains elevated even as the Fed continues to raise rates, sparking concerns that a recession may be unavoidable. A so-called “soft landing” looks further and further out of reach. Consumers have jobs as the labor market remains tight, but consumer sentiment is near record lows according to the Consumer Sentiment Index. 2022 is shaping up to be very different from what our data revealed for the holidays in 2021 last year.With so much uncertainty, what 2022 holiday shopping predictions and insights can we glean from the past and present?

Holiday shopping seems to begin a little earlier every year. In 2022, there’s an economic motivation that is bolstering that trend. Rarely have economic and financial indicators moved as fast as they are right now, and the economy we have now could be very different from the one we have in two months.

Retailers and brands are incentivized to act earlier on two fronts. First, they are concerned about their own rising costs. They will aim to secure shopper purchases earlier with only limited discounts to protect profitability. Second, as shoppers draw down on cash reserves, their appetite to spend in two months may not be as strong as it is now. Locking in shoppers’ intended purchases before household finances feel more pressure could give early movers an edge among brands and retailers alike. This “early bird gets the worm” strategy could be part of the reasoning for the timing of “Prime Day 2.”

On the other hand, shoppers are concerned about inflation and want to start looking for deals early before prices rise further. According to NRF’s latest consumer survey, 44% of holiday shoppers say it’s better to purchase gifts and other seasonal items now because they believe inflation will continue to impact prices later in the year. Shoppers and retailers are locked in an uneasy dance heading into the holidays with both sides eager to make a transaction.

However, one side wants to find deals, while the other wants to withhold them to boost revenue for high-demand categories. We’ll be keeping a close eye on if discounts rise substantially for the period or not.

Despite retailers’ best efforts, retail growth is shifting. The pandemic saw a shopping boom that lasted two holiday shopping periods. The next comparable period will necessarily decelerate. Nevertheless, few analysts predict an outright decline in sales. Rather, revenue will grow more slowly. Our own data shows the average first party brand experienced 14% growth in retail ecommerce growth in holiday 2021 (figure 1) while official figures put total retail growth for the 2021 holidays at 15%. This year, Deloitte predicts Holiday growth of 4-6% with 12.8 to 14.3% ecommerce growth. Figure 1: Retail ecommerce OPS per brand rises in 2021 vs 2020

With inflation hovering around 8-9%, a 5% growth actually represents a 3-4% decline in volume. Shoppers will likely be buying fewer items than last year even if they are forced to spend more due to rising prices. With rising costs and less volume, brands may be contending with smaller profit margins than in the past. This means fewer gifts, and shoppers who are actually trying to cut back on spending even though inflation are propelling it forward.

Our own data shows retail ecommerce prices are still rising rapidly at 9% in August 2022 year over year (figure 2). Figure 2: Prices continue to rise leading into 2022 holidays as discounts remain low

The good news is that more of this shopping is being done online. After a one time surge of in-store shopping earlier in the year, ecommerce has resumed its upward growth trajectory. After slower growth in Q1, Walmart , Amazon, and Target posted 12%, 10%, and 9% ecommerce growth respectively in their Q2 earnings report. Heading into the holidays, our own data for 2022 reveals that YoY retail ecommerce OPS growth has slowed in recent months and gross unit margin has declined since last year except for some isolated spikes (figure 3). Figure 3: OPS growth down from previous highs as margins contract in 2022

Slower growth and smaller margins pressure everyone, but not every brand or retailer is equipped to handle the challenge equally. Those with more scale and diversified profit centers or even those smaller brands that at least have a clear path to profitability are positioned to come out ahead of the competition on the other side of the holidays.

Retail media is still a maturing industry and is growing rapidly. Ad spend during the 2021 holiday regularly achieved levels 50% higher than the prior year (figure 4). More recently, ad spend soared for much of 2022, though it has taken a dip in August. This shift has been accompanied by an uptick in ROAS (figure 5). Figure 4: Ad spend rises rapidly year over year for the holidays

Figure 5: ROAS dips in August after strong increases in 2022

At the same time, brands may start to favor discounts. Historically, the best discounts are not even around key holidays, when ad spend typically plays a larger role. Instead, the best discounts are offered during off-peak shopping days (figure 6) perhaps to strengthen demand during what would otherwise be a slow period. In our data for back to school shopping 2022, discounting did not increase meaningfully at all. For most retail ecommerce brands, visibility is king, not discounting. Figure 6: Unlike ad spend, discounts spike on off-peak days

However, as recession fears mount, brands may pull back on ad spend in favor of discounts to appeal to price-conscious shoppers, or they may forego some investments altogether to fortify their budget at a time when profitability is key. Vendors are more concerned with efficiency than growth. As we see in our data (figure 7), return on ad spend (ROAS) does not rise with increased spending, even around Black Friday, though it can lift incremental sales significantly. Discounts have been exceptionally low during 2022 for most categories. As inflation remains high, however, shoppers might reward lower prices with more conversion, leading brands to find ways of introducing more price discounts while combatting their own rising costs. For instance, our data shows that discounts did make a slight return for Prime Day in July 2022. Figure 7: ROAS no higher on key selling days, no clear pattern across years

While 2021 had much better inventory leading into Cyber Week than 2020 (figure 8), 2022 may have too much inventory that needs to be offloaded as consumer demand falls for discretionary categories as shoppers are forced to spend more on essentials and groceries. Inventory excesses and out of stocks are likely to vary widely depending on the category this year. Figure 8: 2021 shows much improved holiday inventory levels from prior year

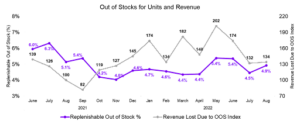

So far in 2022, out of stocks are showing less volatility heading as we head into the holidays vs. earlier in the year (figure 9). Brands can hardly breathe easy however. Too much capacity means excess cost at a time when protecting profitability is crucial. Learning to quickly scale down supply chain costs could be just as important as scaling up capacity was in past years. Figure 9: Out of stocks show more stability ahead of 2022 holidays than in early 2022

All of these metrics we have reviewed vary by category. It’s no surprise that durable categories like home & kitchen sell better than CPG categories during Cyber Week (figure 10), but there are other more surprising trends at work. Office products tend to sell well during the two weeks after Cyber Week. Home & Kitchen sales tend to be depressed before Black Friday. In the week leading up to New Year’s Day, pet and HPC see the most lift vs. other categories. Outside of Cyber Week, brands need to find periods of opportunity they can capitalize on that are unique to their category. Figure 10: Durable goods show the most lift from holiday periods vs. other categories

The beauty category sees big increases in ad spend during Black Friday and Cyber Monday while office, home & kitchen, and even grocery see extended spend afterward (figure 11). Figure 11: Beauty sees early and large ad spend spike during holidays

Office products and home & kitchen see the highest discount levels across the holiday period while tools & home improvement and home & kitchen see some of the biggest spikes on certain days. Christmas Day has more significant discounts than any other day in November and December (figure 12). Figure 12: Home & kitchen and health & personal care show earlier discounts than other categories

For out of stocks, grocery and HPC tend to be the most elevated categories regardless of whether or not it’s the holiday season, but beauty and patio, lawn, & garden can also see significant spikes on certain days throughout the holiday season (figure 13). What does this mean? Brands need to look for hidden obstacles and opportunities that could trip them up, even if they are not on the most important sales days. Maximizing profitability during a time of uncertainty means leveraging data to make the most of non-obvious opportunities that automation and AI employed in retail ecommerce can unearth. Figure 13: Grocery had the most elevated and volatile out of stocks during holiday 2021

In conclusion, how can brands leverage these holiday insights to succeed this season? There are five actions to keep in mind:

Want to learn more about how to plan for this holiday season? Check out our recent webinar on how to plan your assortment for this crucial selling period. Access it here: https://hubs.li/Q01pdZSf0

A note on all CommerceIQ data presented in charts below: the horizontal axis is measured as the number of days removed from that year’s Black Friday which is at 0. The chart stretches roughly from the beginning of November to the end of December for both 2020 and 2021. Data is taken from CommerceIQ 1P customers on Amazon.

Resources

Discover the latest trends in Consumer Packaged Goods

1450+

retailers

100+

mobile apps

59

countries

250+

engineers and

data scientists

Try CommerceIQ

CommerceIQ is the only sales-focused, unified platform built specifically for ecommerce—combining sales, media and shelf data with role-specific AI teammates that deliver actionable, commerce-ready insights.

.png)

.png)